When a U.S. or European hockey player signs a contract with a Canadian team, taxes are usually one of the first concerns—and for good reason. Canada’s top marginal tax rates can exceed 53%, which can feel steep compared to many U.S. states. But what some players don’t realize is that Canada also offers one of the most powerful planning tools available to professional athletes: the Retirement Compensation Arrangement (RCA).

When structured properly, an RCA can serve two important goals at the same time:

⦁ A significant tax-savings strategy, and

⦁ An exceptional forced-savings mechanism during peak earning years.

What Is an RCA?

An RCA is a Canadian trust established through an addendum to the Standard Player Contract (which the CBA permits). Instead of receiving all compensation as current salary, a portion—often up to 49% of total pay—can be deferred into this trust. Although the RCA is a Canadian trust, the investment assets can be managed in the player’s home country (such as a custodian like Charles Schwab in the U.S.), and treated as a grantor trust for U.S. tax purposes. In practical terms, U.S. tax authorities still view the player as owning and controlling the assets.

RCAs generally make the most sense for professionals who do not plan to retire in Canada after hockey. Also, don’t let the word “Retirement” within the RCA acronym scare you. Unlike some retirement accounts in the U.S. where restrictions exist on withdrawals prior to age 59.5, the RCA for hockey players is often a temporary tool for only the time period while competing in Canada. RCAs aren’t limited to players either. Coaches, general managers, and other team personnel working in Canada may also be eligible.

In an effort to explain the benefits and mechanics of RCAs in plain English, the following pages will walk through a simplified, hypothetical example. I will leave the cross-border tax and legal details to the skilled hockey-specific CPAs and attorneys that our office works closely with. In real world practice, RCAs need to be handled with extreme care. Therefore, please ensure you are coordinating with your legal, tax and financial professionals before taking action.

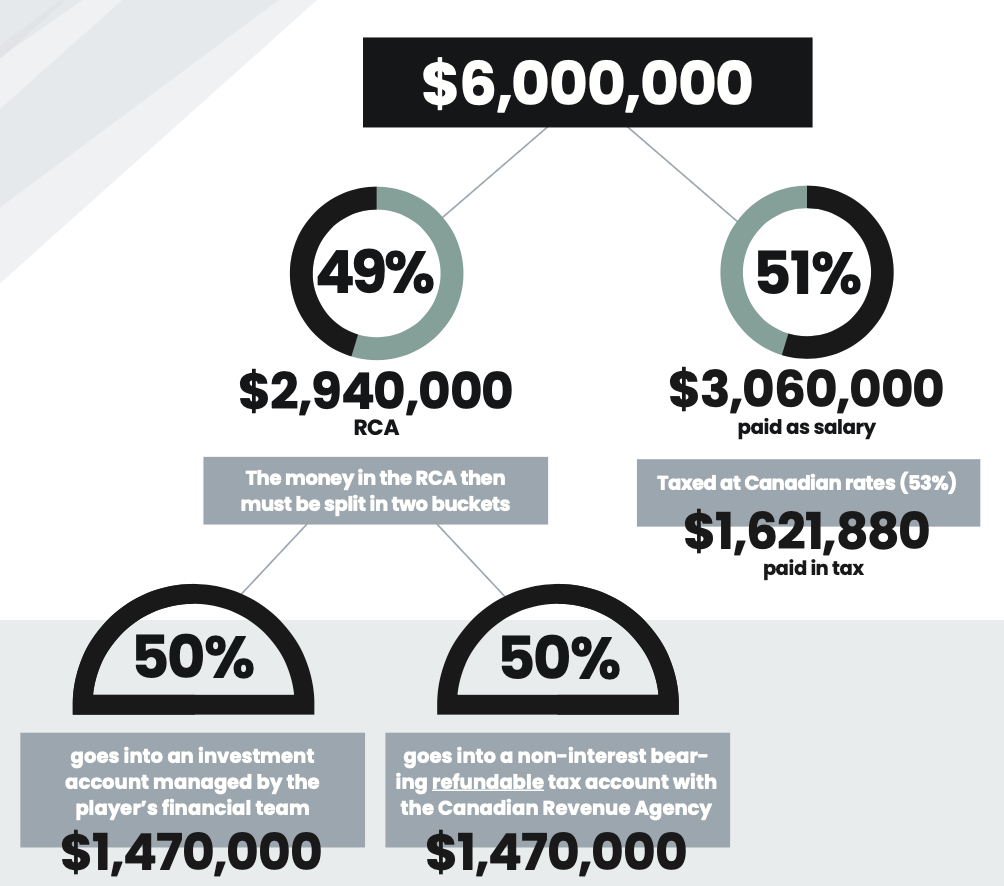

Example: $6,000,000 NHL Contract in Canada (No RCA Planning)

For our example, let’s use a one-year, $6,000,000 contract with a Canadian NHL team.

If no planning is done and an RCA is not used, the tax math in Canada is unfortunately pretty straightforward. As of this newsletter (2026), many Canadian provinces have a combined top marginal tax rate of roughly 53.5%. To keep the numbers easy to follow, we’ll round slightly and use 53%.

At that rate, a $6,000,000 contract would result in approximately $3,180,000 (53%) being paid to the Canadian Revenue Agency. Keep that number in mind as we walk through the alternative.

Now let’s look at the potential use of an RCA, where 51% of the contract is paid as salary and 49% is deferred into the trust:

How an RCA Works: Canada vs. U.S. Tax Treatment

At this point, there’s one key concept you need to understand for an RCA to make sense: Canada and the United States treat these accounts very differently. That difference in tax treatment is exactly what creates the planning opportunity—but only when everything is coordinated properly. Let’s assume the player in our example is a U.S. born player who has signed a contract north of the border.

⦁ From Canada’s perspective, an RCA is a tax-deferred vehicle.

⦁ While the portion of salary paid directly to the player is taxed immediately at roughly 53%, the amount deferred into the RCA trust is not taxed in the year it is contributed. Rather, Canada taxes the RCA upon withdrawal (at a rate of 25% for a non-resident of Canada).

⦁ From the U.S. perspective, the RCA is not tax-deferred at all.

⦁ The IRS does not recognize an RCA as a tax deferred vehicle, which means the entire $6m of contract value in our example is considered taxable income in the U.S., even though a portion was set aside inside the RCA.

U.S. State Residency Considerations & Foreign Tax Credits

For U.S.-born players, state residency can quietly become one of the most important planning decisions of the entire strategy. While the full $6,000,000 contract is subject to U.S. federal tax, it may also be subject to state income tax depending on where the player is legally domiciled—and that difference alone can mean hundreds of thousands of dollars each year.

For example, imagine our player establishes residency in Florida the summer before heading to Canada by purchasing a home and obtaining a Florida driver’s license. Because Florida has no state income tax, his earnings would only be subject to U.S. federal tax. At today’s top federal rate of 37%, that would result in approximately $2.2 million of U.S. tax—significantly less than if he were living in a high-tax state such as California or New York.

Does the player in our example actually need to write a check to the U.S. Treasury for that $2.2 million tax bill? Fortunately, no – and this is where understanding the basics of foreign tax credits becomes so important.

A foreign tax credit allows you to reduce your U.S. tax bill dollar-for-dollar for income taxes you’re paying to another country, helping prevent the same income from being taxed twice. While the real calculation is more nuanced than what follows, this simplified example illustrates the concept of calculating the credit:

$1,621,800 of tax paid to Canada on the salary not deferred into the RCA

+$735,000 of future tax to be paid as Canadian non-resident tax (25% of the $2.94m RCA deferral)

$2,356,800 Total Foreign Tax Credit

In this case, that credit more than offsets the entire $2.2 million U.S. federal tax bill, meaning no additional federal tax would be due. Any excess credit may even help reduce state taxes in certain jurisdictions, which again highlights why establishing residency in a tax-friendly state can make such a meaningful difference.

During the Life of the RCA

Recall that the portion of salary deferred into the RCA Trust is split into two buckets:

⦁ 50% into a non-interest bearing refundable tax account held by the Canadian Revenue Agency

⦁ 50% into the Trust’s investment account that can be managed in the taxpayer’s home country

⦁ Because the United States does not recognize the RCA as a tax-deferred vehicle, the investment side behaves much like a regular brokerage account for U.S. tax purposes. Dividends, interest, and realized capital gains are reported annually and flow through to the player’s personal tax return. As a result, the portfolio should generally be managed with tax efficiency in mind, emphasizing low turnover and minimizing unnecessary realized gains.

⦁ It is easy to forget that the 50% held by the Canadian government is still part of the RCA! Therefore, from an asset allocation standpoint, there is a strong case to be made that the investment portion of the RCA could be allocated to 100% globally diversified equities in an effort to create an aggregate 50% stock, 50% “fixed” portfolio.

⦁ The investments in the RCA should be liquid (no alternatives, no life insurance, no real estate)

Unwinding the RCA: Distribution After Leaving Canada

A player will not want to unwind their RCA until their employment with their Canadian team ends, and they are no longer considered a Canadian resident. Withdrawing funds while still living in Canada can trigger full marginal Canadian tax rates—similar to regular salary—which largely defeats the purpose of the strategy. If a player happens to sign a new contract with a new Canadian NHL team, a second RCA should be considered, as the existing RCAs cannot be merged.

Once the player has returned to the United States, the total value of the RCA is calculated, combining both the refundable tax account held by the Canada Revenue Agency and the investment account. At that point, Canada applies a flat 25% non-resident withholding tax, and the remaining 75% is distributed to the player.

To keep our example simple, let’s assume the investment account experienced no growth during the year. That would leave the RCA balance at $2.94 million. Upon distribution, approximately $735,000 (25%) would be permanently collected by the Canadian Revenue Agency, with the remaining $2,205,000 million paid directly to the player.

Importantly, remember that from a U.S. tax perspective, the RCA contributions were already included as taxable income in the year they were placed in the trust. Therefore, the entire RCA withdrawal is simply a return of capital and a tax-free transfer out of the trust.

Comparing Outcomes: With vs. Without an RCA

If you think back to the beginning of this example, a player earning $6 million in a 53% tax province and doing no planning would simply pay the bill—roughly $3.18 million to taxes—keeping less than half of the contract.

By contrast, using an RCA meaningfully changes the outcome. In our scenario, the player received just over half of the contract as current salary and paid approximately $1.62 million of tax on that portion, then later paid $735,000 of Canadian non-resident tax on the deferred RCA funds. In total, that comes to about $2.36 million of taxes, or roughly 39% of the contract.

That difference—more than $800,000 in this simple one-year example—is real money that stays in the player’s pocket rather than going to the government.

Beyond Tax Savings: The Forced-Savings Advantage of an RCA

While much of this newsletter has focused on the tax advantages of RCAs, there is an arguably even more valuable benefit: they serve as a built-in, forced savings mechanism during a player’s peak earning years.

The business side of hockey can be unpredictable and shrewd, and careers often end sooner than anyone hopes due to trades, injuries, or circumstances outside your control. By automatically setting money aside before it ever hits a player’s checking account, an RCA helps ensure that a meaningful portion of today’s income is protected for tomorrow, turning short-term success into long-term security.

Questions About RCAs for Canadian NHL Contracts?

As always, if you have questions or would like to explore whether an RCA makes sense for your situation, our team is here to help. We’re happy to serve as a resource for you and your family and can coordinate with the appropriate tax and legal professionals to thoughtfully implement a strategy that fits your goals.

Johann Kroll, CFA, CFP®

Founder

Investment services offered in Canada are provided through The Hockey Wealth Group Canada LLC, a registered portfolio manager in Canada. Investment services offered in the United States are provided by Oceanside Advisors LLC dba the Hockey Wealth Group, an SEC registered investment advisor. The information in this newsletter is for educational purposes only and does not constitute financial, tax, or legal advice. Past performance is not a guarantee of future results. Any performance numbers in this newsletter do not include the impact of taxes, fees, and inflation. All strategies should be coordinated with the appropriate tax, legal and investment professionals.